Retirement Philosophy

Retirement Revolution

In the last several years the science and art of retirement planning has made revolutionary advancements. The latest research is proving to totally refute the traditional methods of retirement planning.

If you are retired or within 10 years of retirement you have probably asked yourself several questions about the future of your retirement. Some of these questions may include:

- Do I (Will I) have enough money to retire?

- How long will my money last?

- How much of my savings can I use without risking my future?

- When can I retire?

- How will downsizing my home help my retirement?

- How much do I need to save for my retirement?

- Are my investments optimized for the best outcome possible?

Traditional Method of Retirement Planning: The traditional method of retirement planning forecasts the longevity of a retirement portfolio (distribution portfolio) based on the average or assumed portfolio growth, retirement income need, inflation rate, and expected lifespan. If the actual events unfold below the average the plan may fail.

Advanced Retirement Planning: On the other hand, the new “Advanced Retirement Planning” techniques are based on engineering principals that calculate the ability of a portfolio to provide lifelong income under adverse conditions. This is best understood using an engineering example:

"When an engineer builds a skyscraper, he does not build it to withstand the average wind velocity. The engineer designs the building to withstand the strongest wind velocity. Otherwise, an above average wind could bring down the building."

Unfortunately, most retirement planners and planning software programs allow the user to input their own assumptions or to use simple averages. If a retiree’s portfolio experiences anything less than average, their plan will fail.

Instead of presenting a "forecast" of a client's future financial picture based on unreliable assumptions, we produce a potential outcome based on actual market history. In addition, we "stress test" the historic outcomes to determine the ability to withstand a wide range of adverse events and conditions.

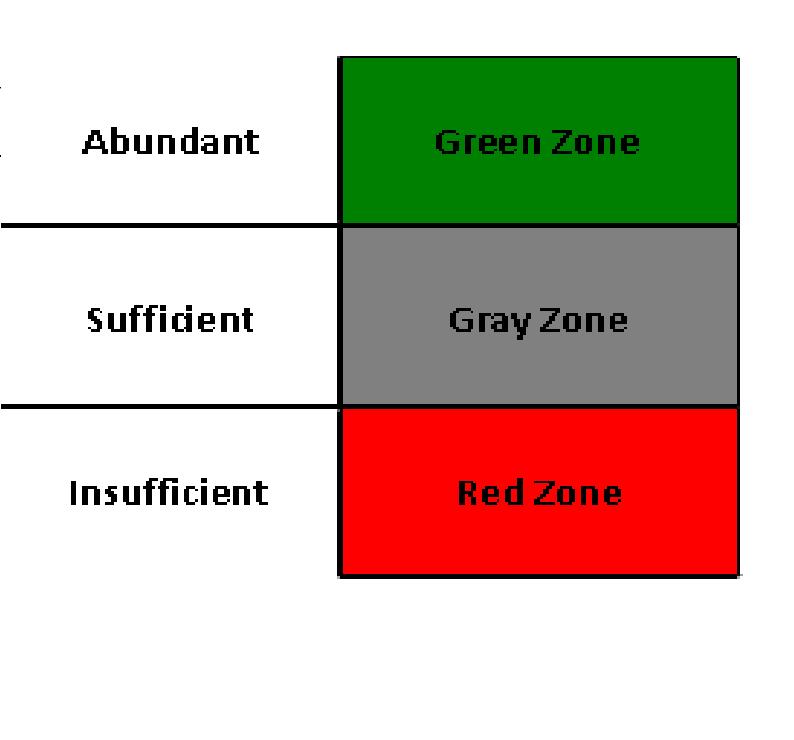

While our calculations may be complex, our goal is straight forward; to realistically determine how much is enough to lifelong income? The results of our analysis are categorized into three simple zones:

Green Zone - Abundant resources for lifelong income

Grey Zone - Sufficient resources for lifelong income

Red Zone - Insufficient resources for lifelong income (more planning is required)

If you are retired or within 10 years of retirement a financial analysis of your retirement outlook may be the most important calculation you make. It not only reveals your current outlook of success but it offers options, instructs decisions, and optimizes investment composition.

A miscalculation of your retirement reality could have a devastating result later in life, when you are at your most vulnerable. This is why we consider retirement planning and retirement management a service that demands the highest possible standard of trust.